Funding the startup of a new dairy operation or the transition of an existing farm can be a tall task for any producer. Remember the “five C’s of credit” – a checklist of factors for producers to consider when securing funding for an agricultural business venture.

The five C’s are widely used by lenders of all types. Each organization may prioritize them differently, but virtually all lenders will consider them when evaluating a loan request.

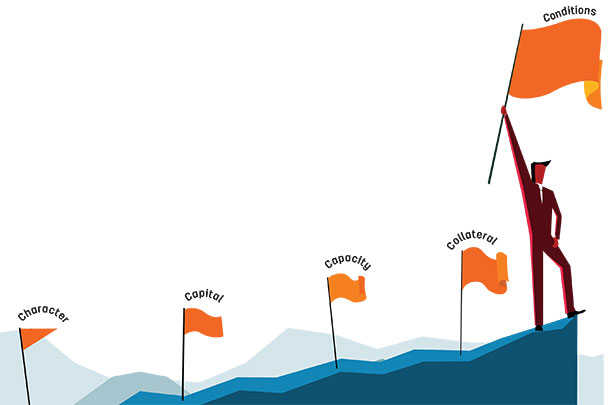

1. Character

In the absence of a long financial history with a lender, a young or beginning producer will likely need to demonstrate strength of character in building a financial relationship. Honesty and integrity may be cliché, but in this context, they are critically important in securing financing.

A lender must have confidence the producer will act with honesty and maintain communication throughout the term of financing. One tool often used to evaluate character is your credit report. Obviously the entirety of one’s character is not contained in your credit score, but it is an indication of how you have handled credit in the past and an important consideration for most lenders.

2. Capital

While many lenders put a lot of stock in a young or beginning producer’s character in entering into a financial relationship, they know capital may be in shorter supply. In most cases, a young or beginning producer simply may not have the assets or access to capital compared to a more established producer.

Character becomes a more critical piece in the absence of significant startup capital. In general, lenders want to see that you have “skin in the game,” are putting up some of your own money, and not relying solely on their resources to finance your business.

One of the metrics some lenders use when evaluating dairy loans is debt per cow. While each lender may have a different comfort level regarding debt level, this can be an important measure for an appropriate amount of leverage.

3. Capacity

In short, this is a producer’s ability to generate earnings that can be used to repay a loan. It refers to a producer’s track record of working and managing his or her business prior to seeking financing to start a new agriculture venture.

A good example is a young producer who can show proof he or she has worked for others on a smaller scale, has made payments on existing assets, and can demonstrate a thoughtful plan and financial commitment to his or her goals. It does neither a borrower nor a lender any good to extend credit beyond an individual’s capacity to repay that debt.

In a commodity-driven business like dairy, external conditions, such as milk price, are a major factor in repayment capacity. However, management plays a significant role as well. Are you consistently in the top tier of profitability? Or has your farm struggled to turn a profit, even when prices are relatively good?

4. Collateral

Collateral is the lender’s safety net. Like capital, collateral is often in short supply for young or beginning producers. Typically, leasing or renting property is a good way to build a footprint in the farm sector.

Not only is that a good way to build a business model, it’s also a better approach for a young producer whose plans and aspirations may not be chiseled in stone. Much like capital, a young or beginning producer likely won’t have the collateral of a more established producer, making it important to demonstrate a commitment to building a positive repayment history as his or her relationship with a lender evolves.

5. Conditions

If starting an operation from square one, a young or beginning producer may seek different financing conditions to account for startup costs and a lack of initial production. Financing that requires interest-only payments for the first year, or delaying payments altogether, could be options to help a young producer get a crop in the ground that may not begin producing until year two, for example.

Being able to demonstrate he or she will start making more substantial loan payments once production is underway is another way to instill confidence in a lender.

In addition, a lender may require conditions of their own as part of the deal. A common one is the use of a loan guarantor. A cosigner or a guarantee from an agency such as the USDA’s Farm Service Agency could be required for a borrower who is short on collateral or has other weaknesses in their credit profile.

Although these five C’s are important for young or beginning producers to consider when seeking financing, it’s just as important to be open, willing to communicate and learn, and embrace new opportunities.

One factor in a young producer’s future success is his or her willingness to listen to the counsel of a loan officer or other financial advisers. It’s very important for people starting out to surround themselves with a network of trusted advisers and to listen to them – even when the advice may not be what you want to hear.

Knowing the five C’s and where you stand on them will help you to consider the lender’s perspective when having discussions about financing your enterprise. Remember, any lender is primarily concerned with your integrity, your ability to repay the loan and managing their risk. They want you to succeed as much as you do. ![]()

ILLUSTRATION: Illustration by Thinkstock.

-

Chris Laughton

- Director of Knowledge Exchange

- Farm Credit East

- Email Chris Laughton