“What a difference a year makes.” It’s a phrase we’ve heard a million times, yet at least in the agriculture industry, those words could not be any more true. Dairy producers have seen a swing in Class III milk prices of greater than $8 per hundredweight.

In today’s economy, dairy producers are really having to focus on reducing the “three C’s”:

- Cost of production

- Capital expenditures

- Cash expenses (most important)

As lenders, we see a lot of different scenarios play out when clients are faced with declining milk prices and tighter margins than they’ve experienced over the past few years. Three common scenarios are:

- Full utilization and discipline when using revolving lines of credit with their bank

- Buildup of accounts payable (The two main expenses on a dairy are feed and labor. When cash flow is tight, we need to continue to pay hired labor and therefore unsecured accounts – co-op, seed, vet – can begin to accumulate.)

- Accelerating payments on term or real estate debts early to eliminate the payment, thereby easing up the cash flow requirements

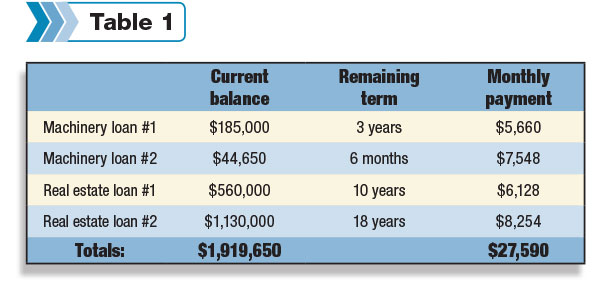

So which option is best? Let’s examine two situations with two different cash-utilization scenarios. First, we need to establish the debt structure for this dairy. Also, for this scenario, I am only discussing the operating revolving line of credit, realizing most dairies of size also have hedge lines of credit or borrowing base cattle loans.

The hedge note should be getting paid as your positions settle and reconciled each month. The borrowing base loan will also fluctuate similarly to the operating revolving line of credit.

When prices were high in 2014, many of our clients paid the principal balance on their revolving credits down to zero and then began making accelerated payments on their term and real estate debts.

They saw the advantage of reducing debt and interest expense. In Table 1, these producers probably would have paid off machinery loan No. 2 and possibly made extra payments on remaining loans.

We typically encourage clients to “work down your balance sheet” by paying off revolving lines of credit first, followed by term loans, and the last loans to pay off would be real estate.

Why pay off revolving credits first? Because you can always borrow that money back without having to refinance your current loans, which often results in additional loan fees.

This is truly utilizing the flexibility of the lines of credit as they were intended by reducing interest costs and paying them down with extra funds to have the commitment available to borrow as cash flow dictates, either for bill payment or prepaid expenses to take advantage of cash discounts. Next, pay off term debts, as those assets depreciate faster and need to be replaced.

Examining the benefits of accelerated payments

If your dairy was able to accelerate your payments by an additional $6,000 per month for a year in the above examples ($1,000 on each term note, $2,000 on each real estate loan), what would the financial implications be? Your interest cost would be reduced by only $1,581 that year.

Recognize some additional principal will be paid down, but after $72,000 of payments, your interest cost for that year only dropped by $1,581. I want to reiterate, this option should only be considered after revolving debt has been paid to zero.

Now that we are in lower milk prices, is it advantageous to keep the accelerated payments on those loans – which may cause accounts payable buildup – or revert back to the required payments? Is there a better use for the $72,000? The answer is yes. Stop the accelerated payments and apply that $72,000 towards your line of credit or accounts payable.

If you build up accounts payable, they may charge up to 18 percent APR which, in the same time frame of a year, will cost you $12,960 additional interest. This does not factor in the cash discounts you are missing out on and you cannot put a price on the benefits of having the additional working capital on your operation.

The statement we have all heard is: “Cash is king.” In a market like you are facing, you may need quick access to cash through assets that are easy to liquidate. Working capital will be a key factor in determining how you weather the storm, as it were. Remember, working capital is the difference between current assets and current liabilities.

Paying down on your line of credit instead of accelerated payments will allow you additional borrowing capacity in the future that will assist you in keeping current on bills and avoiding the 18 percent APR by unsecured creditors.

Of course, the next step is to protect the working capital you have by making sound capital purchase decisions, utilizing risk management, fixing interest rates, etc., to allow you the flexibility your operation will need.

Having adequate working capital of $600 per cow should be a factor you and your lender consider when evaluating your financing needs.

If we go back to the three scenarios of how to handle tight cash-flow situations, the preferred option would clearly be option No. 1 to fully utilize your revolving lines of credit. If you do not have a revolving line of credit with your lender, ask what you need to do to obtain one. It is critical to show your lender that you have the discipline to revolve it and make payments.

Lastly, if your line of credit is fully extended, sit down with your lender and look at a burn rate of your working capital and possibly set up a working capital loan for 2016. How do you calculate a burn rate in a loss year?

If you are projecting a loss for 2016, divide your working capital by the expected loss. For example, if your working capital is $750,000 and your projected loss is $200,000, you have 3.75 years of working capital available.

If your burn rate is less than three years, talk with your lender on decisions you need to make today and begin monthly cash flows and compare budget to actual. Remember, however, to look at how liquid your working capital is. If the majority of your working capital is feed, how easy will that be for you to convert to cash when you have cows to feed and bills that need to be paid?

The key is avoiding impulsive emotional decisions today to try to fix your cash flow when it could be a decision that will negatively impact your operation down the road. Make sure you and your lender have a solid plan to set your operation up for success long-term. Wishing you all a safe planting season and, mainly, thank you for what you do every single day to feed America. PD

For more insights from Lori and other AgStar experts, check out AgStar Financial Services, ACA, where you’ll find livestock and grain industry news, legislative happenings, and financial preparedness guidance.

Lori Teigen is a senior financial services executive at AgStar Financial Services. Lori grew up on a registered-Holstein dairy farm in New Richmond, Wisconsin.

She received her Bachelor’s degree from University of Wisconsin – River Falls with a double major in business administration and marketing communications. Lori started with AgStar in December of 2003 and is now working with clients on their lending and insurance needs. Email Lori Teigen.