September back to ‘normal’

September FMMO class prices, with comparisons to August, were as follows:

- Class I base – $18.44 per hundredweight (cwt), down $1.34

- Class II – $13.16 per cwt, down 11 cents

- Class III – $16.43 per cwt, down $3.34

- Class IV – $12.75 per cwt, up 22 cents

Although mostly lower, milk class prices fell into more traditional patterns in September. The Class I base price was higher than the Class III price for the month.

Also, the spread ($3.68 per cwt) between the September Class III and Class IV milk prices narrowed to its smallest gap since May, down from $8.14 per cwt in June, $10.78 per cwt in July and $7.24 in August.

The value of protein in FMMO price formulas weakened by more than $1 in September to $3.39 per pound. In comparison, the butterfat value declined just 4 cents to $1.59 per pound, contributing both to the lower milk price but also the much narrower spread in Class III-Class IV prices.

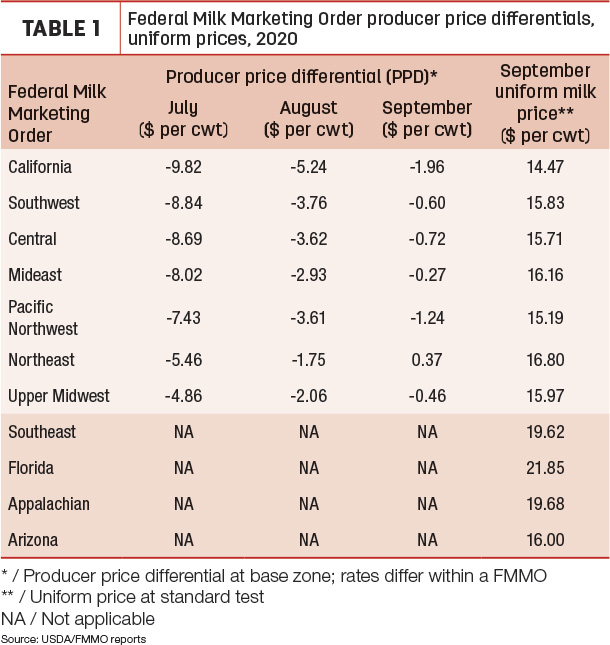

With three of four milk class prices lower, September uniform milk prices were lower than August prices in 10 of 11 FMMOs (Table 1). Month-to-month declines ranging from 6 cents in California to $1.74 in the Upper Midwest. Only the Arizona FMMO posted a small (16 cent) increase.

A look at the pools

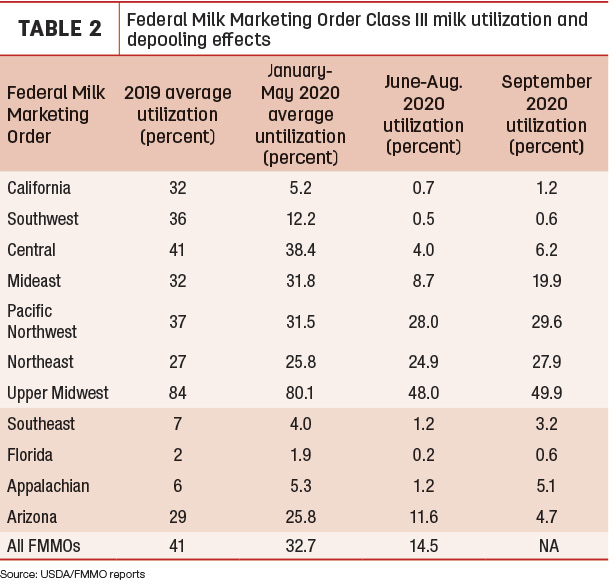

September Class III utilization as a percent of all milk uses in each FMMO is shown in Table 2. Based on historical patterns, a little more Class III milk rejoined the FMMO pools in September compared to peak depooling months of June-August.

Through the first five months of 2020, Class III milk pooled in all 11 FMMOs averaged more than 4.34 billion pounds per month. With heavy depooling in June-August, the volume of Class III milk pooled across all 11 FMMOs averaged just 1.45 billion pounds per month. In September, Class III pooling was estimated slightly higher at 1.73 billion pounds.

PPDs improve

The extreme inversion in Class I base-Class III prices and a wide gap between Class III and Class IV milk prices early this summer led to widespread depooling and historically negative PPDs. With more normal milk class price relationships, the September PPDs in the seven FMMOs using multiple component pricing formulas moved higher (Table 1), improving $1.60-$3.28 per cwt from August. (As we’ve noted previously, PPDs have zone differentials, so they’ll vary slightly within each FMMO.) Although PPDs remained negative in six of those FMMOs, the PPD actually moved to the positive (37 cents) in the Northeast.

October more ‘scary’

The ghost of more negative PPDs is likely on October milk marketings. Here’s why.

The USDA has announced the October 2020 FMMO Class I base price at $15.20 per cwt, down $3.24 from September.

October’s FMMO Class II, III and IV milk prices won’t be announced until Nov. 4. However, as of Oct. 15, October Chicago Mercantile Exchange (CME) Class III milk futures closed at $21.32 per cwt, about $6.12 per cwt higher than the announced October Class I base price. And the expected gap between Class III and Class IV futures prices will widen in October: As of Oct. 15, the CME October Class IV futures price closed at $13.53 per cwt, $7.79 per cwt under the Class III price.

Propelling Class III milk futures higher, CME cheddar block cash prices moved to $2.72 per pound on Oct. 14-15, spurred on by September’s USDA announcement of a third round of Farmers to Families Food Box Program contracts.

Thus, the protein value will go up, adding support to prices. However, the Class I-Class III inversion will return and the Class III-Class IV price gap will widen, creating incentives for depooling and negative PPDs, quite possibly into the new year. What impact that has on your milk check depends on your individual milk handler.

Read also: Impact of the farm bill change to the Class I milk price on dairy farm income. ![]()

-

Dave Natzke

- Editor

- Progressive Dairy

- Email Dave Natzke