Say it however you choose, but my grandma got a lot of mileage out of the line: “Don’t count your chickens before they hatch!” As grain prices have eroded, many producers have gotten excited about the opportunities before them.

They are waiting out the lower feed prices with the idea that the milk prices currently viewed in the futures market will be there when the milk check hits the mailbox. Those chickens haven’t hatched. It is time to be very objective about our margin opportunities as we view them.

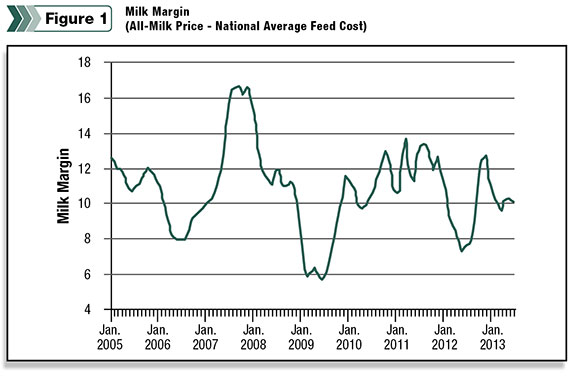

Using Penn State’s feed price formula to calculate spot feed prices and the all-milk price, one can track margin history.

Obviously there are many variables from farm to farm, but use of this information allows us to make general conclusions.

To that end, a quick glance at the milk margin chart ( Figure 1 ) offers some insight into what is considered normal.

First, you will notice that low periods in margin tend to occur every three years. In the past, this trend was largely defined by milk price.

The greater amplitude of volatility in today’s feed costs has allowed them to play a greater role. Nonetheless, the three-year pattern continues.

Secondly, margins generally tend to range from $8 to $12 per hundredweight (cwt). While we can begin to become optimistic about the future when margins are around $8 per cwt, it is also true that we should be preparing for margins to decline when they are near $12 per cwt.

At present, margins are approximately $10.15 for spot prices. Looking forward, margins for next spring are near this same level.

While in the middle of the historical margin range, amid the growing likelihood of lower feed prices and great uncertainty surrounding the future of milk prices, we must be cautious to manage margin risk without compromising future opportunity.

How do we address such a scenario? First, let’s tackle feed. Much movement has been made toward lower prices in recent months as we advance toward harvest. Take advantage of the opportunity to capture seasonal opportunities as harvest approaches.

Book feed forward through next summer unless local opportunities are being presented that offer greater benefit. While the bias may be for plentiful feed supplies, there will still be some areas where supply will be tighter than normal.

Generally, the best time to take advantage of prices in such areas is at harvest, when basis is weak and supply is momentarily abundant.

Purchases at harvest will allow you to avoid the possibility of delayed or absent availability of product and eliminate the possibility of a local price-basis squeeze prior to next year’s harvest.

If there is reason to believe that there is still more opportunity to see lower prices at a later date, defend your harvest purchases with put options. If you are tied to a pricing arrangement that doesn’t allow you the ability to lock in prices, use call options to defend against any winter or spring rallies.

Contact your risk management adviser to develop an appropriate strategy for your situation.

Now, the trickier of the two … milk. The “three-year cycle” would suggest that moderate prices would prevail in the coming year. However, with the disruption of droughts, both here and New Zealand, price cycles are a bit askew.

As we work through all of the necessary adjustments, milk price will remain at the mercy of a number of factors, such as world weather, global economic conditions, demand from southeast Asia and the value of our currency, to name a few.

All of this is to say that milk price is fairly unpredictable as we head into 2014. This is exactly why a strategy that provides flexibility is in order. With regard to that strategy, a producer’s level of risk aversion in combination with historical margin trends should define how they respond to the current environment.

As illustrated earlier, we are currently in the middle of what would be our historic margin range.

Mindful of that, if you find yourself in a margin situation whereby your projected return is one that you are unwilling to even fractionally part with, you should (in conjunction with your feed purchases) consider a sale of milk to either your buyer or through a futures contract.

Before using a futures contract, please understand the market exposure that accompanies that activity prior to initiating it. That sale can then be defended with call options that allow you to participate in any large upward movement in milk prices.

While the cost of the call strategy will require spending a portion of the projected margin, it is definable. Without a call strategy, any potential improvement in margin is lost after the sale is made.

If you find yourself willing to risk a portion of your projected margin for the opportunity to see better milk prices, a put option strategy would be a better approach.

You will have protected your margins from falling milk prices, and by default, allowed for improvements that may come down the road.

Finding yourself in the middle of historical price ranges is difficult for any manager. Many are often left with the deer-in-the-headlights look and do nothing. That can work well or hurt equally as much. Instead, a flexible approach to managing milk revenues and feed costs is in order.

Manage the middle of our current margin range with the use of options so as to not count your chickens before they hatch. PD

In compliance with Dodd Frank legislation, this article must be considered as a solicitation for your business.

UPDATE: Since the publication of this article, Mike North has left First Capitol Ag and is now the president of Commodity Risk Management Group. Contact him by email .

Mike North

Senior Risk Management Adviser

First Capitol Ag