Recently, the Class III futures for the upcoming months trading on the Chicago Mercantile Exchange (CME) have experienced some downward volatility that has eroded much of the narrow profit potential for dairymen.

After talking with several producers who are busy with this year’s plantings, I realized that the market changed so quickly that many producers were unaware of the significant drop in price.

In order to get a little different perspective on market volatility, I did some analysis of the Class III futures market to see if the market has frequently made notable changes within a couple months.

Let’s look at some of the most extreme milk prices in recent years and examine how those months traded prior to settlement. For each month, the Class III milk price trades on the CME for up to 24 months before the contract settles.

During that time producers have the opportunity to trade that contract and protect their milk price at the current trading levels; otherwise, the producer price is based on the USDA-announced settlement price.

Below are a few examples of extreme milk prices and the drastic changes that occurred in the CME futures trading prices prior to settlement.

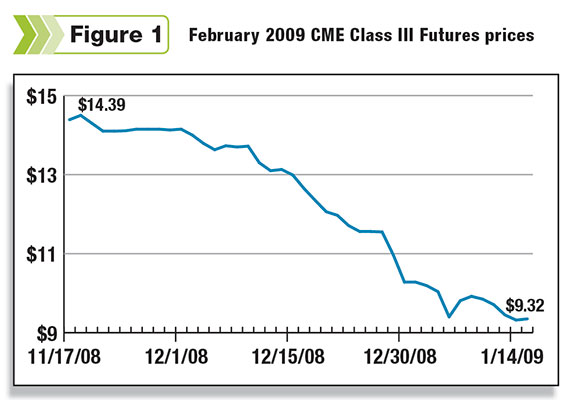

February 2009

The USDA announced settle price for February 2009 was $9.31 (see Figure 1 ), which was the lowest Class III price in recent history.

That price was devastatingly low for producers across the country.

For some, the most painful part of the February milk price was knowing that they could have protected their milk price at a higher level, but ultimately no action was taken. During the summer of 2008, the February 2009 Class III futures price traded up to approximately $20.50.

Unfortunately, over the next seven months the Class III futures price for February 2009 declined roughly $11 per hundredweight (cwt). Most of the decline occurred at a moderate pace, consistently moving lower over time.

The quickest change occurred between mid-November and mid-January, when the Class III futures price declined approximately $5 per cwt.

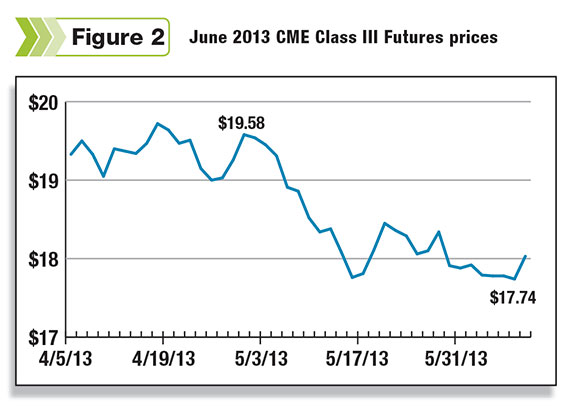

June 2013

More recently, the June 2013 Class III futures price declined rapidly in a five-week period from the end of April 2013 to the beginning of May 2013 (see Figure 2 ).

Within that time period, the Class III futures price for June declined about $1.80 per cwt.

The decline in the June Class III futures price stood out to me because many producers were comfortable with the June futures trading price in April, and therefore content to be in the cash market (not hedged).

In fact, many producers became so comfortable with the price and the market that they became busy with spring planting and didn’t even notice that the price had declined nearly $2 in just over a month.

With higher feed costs across the country, many producers are seeing a breakeven Class III price that may be at or even above $18 per cwt. The June 2013 Class III price that was trading back in April could have provided an income for many producers that would have met or exceeded their cost.

Unfortunately for many of those producers, as the price eroded so did their profit potential. As I write this the June price is just over $18, which is down approximately $1.50 from where it was trading earlier this spring.

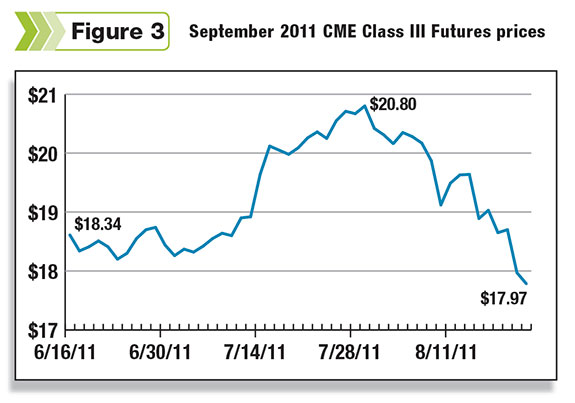

September 2011

I like showing September 2011 (see Figure 3 ) because it was a bit of a roller coaster. Within just two months, the Class III futures price increased approximately $2.50 and then decreased nearly $3.

This is a great chart for producers to review because so often the market starts to move higher, and we immediately think that the risk management strategy was implemented too early.

Yes, it would be great if we could always hedge at the top of the market, but that is not realistic.

Until the contract settles, the market can still move significantly lower, and without a hedge in place, you are vulnerable to the market volatility.

The goal should always be to hedge a price that works for your farm business. Therefore, if prices increase or decrease, you’ll still be making money as a dairy.

So what can you do about these volatile prices? In short, there are two answers: hedge to avoid the volatility or remain in the cash market and be prepared to ride out the price volatility.

Hedge

If you can’t or don’t want to ride the milk price volatility roller coaster, hedge against it through your cooperative, broker or with USDA insurance.

Risk management options are diverse, and there are many professionals who can help guide you through the various strategies to pick the best approach for you and your business.

It is becoming more popular for producers to outsource their risk management needs to an appropriate consultant or broker. The professional will often review the farm’s financials, understand their professional goals and also understand their personal apprehensions.

While this approach is not for everyone, many producers are finding that outsourcing their risk management makes the process less personal and helps get them over the initial hurdle of implementing a strategy.

It also helps to keep their risk management strategy up to date, and the producers don’t have to worry about analyzing the current risk management strategies at the same time they are planting their crops.

Self-insure

After reviewing the farm’s financials and the current risk management strategies, some producers will choose to remain in the cash market and “self-insure” against market volatility.

This is a great approach for producers who have the financial stability to survive a low milk price cycle and also have the personal strength to endure the stress that goes with it.

Unfortunately, price volatility doesn’t appear to be going away, but luckily producers have more choices when it comes to risk management.

The markets can change quickly, and the opportunity that exists today may be gone tomorrow. If you are nervous about what the future may bring, start reviewing your risk management options and talk to the professionals. PD

Krupa is a broker with Chicago-based Rice Dairy, a boutique brokerage firm offering guidance, analysis, and execution services on futures, options, spot and forward markets. She can be reached by email . There is risk of loss trading commodity futures and options. Past results are not indicative of future results.

Katie Krupa

Broker

Rice Dairy