The consumer of dairy products – the person who buys that chunk of cheese, jug of milk, pizza topped with cheese or bakery product with whey solids or milk powder as an ingredient – is who makes the dairy industry a business.

The good news is: The consumption of total dairy products continues to grow (see Table 1). To keep dairy production growing, it is important to know the kinds of dairy products consumers are buying. Are they buying more of some dairy products and fewer of others?

What signals are consumers sending in the type of dairy products they purchase? Annually, the USDA publishes data that helps answer those questions. Let me share with you eight observations that stand out in my review of the most recently released annual consumption data – observations that help us understand which dairy products consumers are purchasing.

What signals are consumers sending in the type of dairy products they purchase? Annually, the USDA publishes data that helps answer those questions. Let me share with you eight observations that stand out in my review of the most recently released annual consumption data – observations that help us understand which dairy products consumers are purchasing.

-

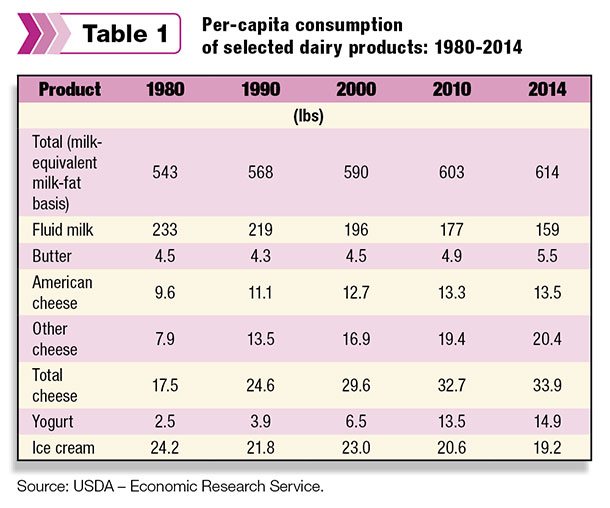

Let’s start with the best news. Per-capita consumption of all dairy products (milk-equivalent milkfat basis) was 614 pounds last year. This makes 2014 the 10th consecutive year consumption exceeded 600 pounds.

We have to go back to the 1960s to find a higher per-capita consumption level. What is more impressive about 2014’s consumption is that it was 9 pounds higher than 2013, and the increase took place in a year with record farm milk prices.

-

Consumers continue to “eat” more and “drink” fewer dairy products. Today, about twice the amount of milk is consumed in the form of cheese compared to fluid milk. In 2014 fluid milk consumption dropped to 159 pounds per capita.

Fluid consumption has declined every year since 1972. Thank goodness consumption of cheese has more than offset the fluid milk decline. Last year saw cheese consumption at 33.9 pounds.

Since 1975, cheese consumption has more than doubled. Households may no longer receive home delivery of milk in fluid form, but they receive it in the form of cheese via pizza deliveries.

-

Starting at the end of World War II and continuing until about 10 years ago, per-capita consumption of butter experienced a long downward trend. Then consumption of butter started trending upward. During the past three years, butter consumption has held at 5.5 pounds per capita.

We have to go back to the mid-1960s to find a higher level of consumption. Granted, 5.5 pounds is still only about one-half the consumption level in 1945, but the trend is upward. With the butter announcement by McDonald’s, and the expectation of others to follow, who knows; it may reach 10 pounds per capita again in the not-so-distant future.

-

Prior to 1986, more whole milk was consumed than reduced-fat or skim milk. In 1986, this changed; more reduced-fat and skim milk was consumed than whole milk. Reduced-fat and skim’s share continued to expand to 73 percent of total fluid sales, with whole milk at 27 percent in 2012.

Now, we are seeing a change. Last year, whole milk sales actually increased from the previous year. Whole milk sales improved to 29 percent of total fluid milk sales. Similar to butter, could consumers be appreciating the taste of milkfat and realizing milkfat may not be bad for one’s health as we have been told? So far this year, the whole milk upward trend is continuing.

-

From 2009 to 2014, organic fluid milk sales increased 54 percent, while during this same period conventional fluid milk sales declined 12 percent. In 2009, organic represented about 3 percent of total fluid sales.

Last year, organic increased to almost 5 percent of all fluid milk sales, with sales approaching 2.5 billion pounds. Organic continues to grow and be a more significant part of total fluid sales. I continue to ask myself what conventional can learn from organic to turn its sales around.

-

With the large amount of grocery store freezer space devoted to ice cream, one would think ice cream consumption is growing. However, the numbers tell a different story. Ice cream per-capita consumption has trended downward since the turn of this century.

The 19.2 pounds of ice cream consumed in 2014 is down more than a pound in just the past two years. Why the decline? One of my reasons for the decline is the reduction in size of ice cream package by many manufacturers from half-gallon to 1½ quarts. The same number of units may be sold, but volume is less.

-

Per-capita consumption of cheese continues to grow, but at a slower rate. During the decade of the 1980s, cheese consumption increased 6.3 pounds from 1980 to 1989. In the 1990s, the increase was 4.3 pounds. During the first decade of this century, growth slowed to 2.7 pounds.

So far in this decade, per-capita cheese consumption only increased 1.2 pounds from 2010 to 2014. Even with slower per-capita growth, increasing population means still more cheese sold every year. However, we probably will not see the significant growth in cheese consumption experienced during the 1980s and ’90s.

-

From 2000 to 2014, per-capita consumption of yogurt increased more than 125 percent, going from 6.5 pounds to 14.9 pounds. It is estimated about 40 percent of current yogurt sales are “Greek-style,” which has boomed in recent years.

Depending upon the process used, Greek-style yogurt utilizes two to three times more raw milk or other dairy ingredients compared to conventional yogurt. The result, the milk needed to produce yogurt has well exceeded the growth in per-capita consumption.

Looking ahead, many dairy marketers think Greek-style yogurt may have reached its plateau, but they expect other types of yogurt will keep yogurt consumption growing.

In summary, per-capita consumption of dairy products continues to grow, which is excellent news for the dairy industry. The types of dairy products consumed have changed over time, and no doubt will continue to change.

The key for all segments of the dairy industry is to stay abreast of consumer changes in consumption and respond accordingly, thus keeping total dairy consumption moving upward. PD

Calvin Covington is a retired dairy cooperative CEO and now does some farming, consulting, writing and public speaking.