Until recently, it was generally accepted that milk prices ran on a three-year cycle: one year of moderate prices followed by a year of very strong prices and then a year of weak milk prices.

This conventional wisdom appears to have been broken. Counting on traditional trends and cycles to continue could be detrimental to a dairy’s future, according to a new Knowledge Exchange Report from the staff at Farm Credit East.

“In dairy, we now must challenge the conventional thinking that we are just a few months away from a return to the three-year cycle and to much better farm prices,” says Tom Cosgrove, senior vice president of Farm Credit East Public Affairs and Knowledge Exchange.

As suggested by the title of the report, “Dairy Industry Reset Post-2014: A Time for Dairy Producers to Take Bold Action,” Cosgrove says dairy producers must view their business through a different lens.

“The industry may well be entering into a fundamentally different pricing and profitability era – a market reset,” Cosgrove says. “Not only could the three-year cycle be a thing of the past, this reset might signal an extended period of restructuring of U.S. dairy farming.”

How do dairy producers, their lenders and others plan for the future when this conventional rule of thumb no longer seems to apply?

“To effectively plan for long-term profitability, manage risk and preserve wealth, producers will need to take bold actions. Hoping for the three-year cycle to lift farm profits is not a viable business strategy,” according to the report.

Eras of dairy

The Knowledge Exchange Report looks at the last 35 years of dairy markets and farm business results, with underlying data compiled from Farm Credit East’s annual Northeast Dairy Farm Summary.

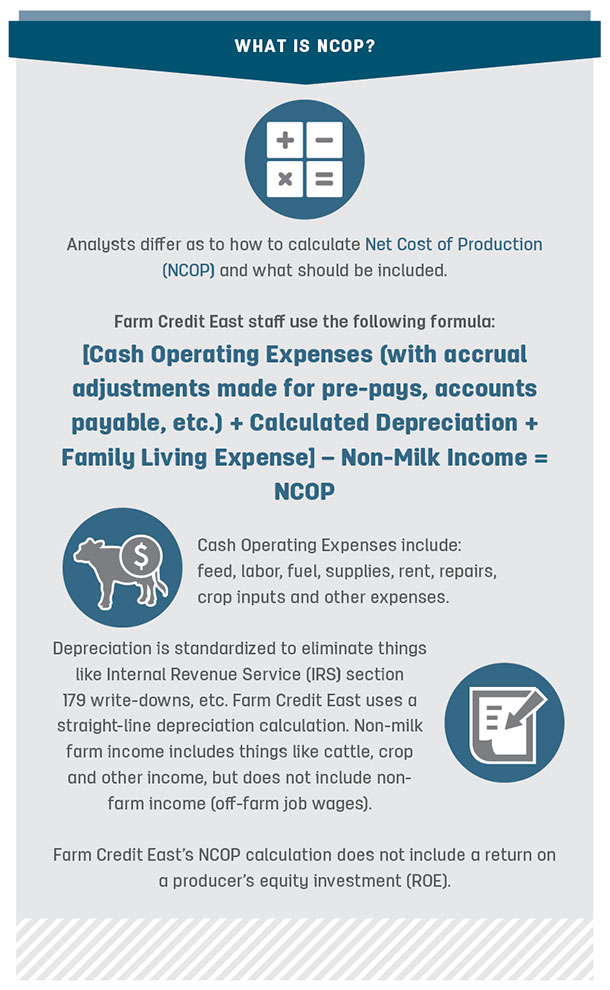

It analyzes Northeast producer returns, milk prices, net cost of production, dairy production capacity and implications for farm debt. It describes three distinct eras since U.S. milk prices were decoupled from the parity price concept in 1981 and unveils a new, emerging era.

- The post-parity era (1981-1995). In 1981, parity pricing was discontinued and the federal milk support price was ratcheted lower. It created a difficult period for dairy producers, leading to significant downsizing as they adjusted to more market-oriented pricing.

Excess production capacity combined with high inflation and high interest rates, leading to poor profitability. Average annual return on equity (ROE) was 0.7 percent. Through the period, the real farm milk price declined by an average of 79 cents per hundredweight (cwt) per year and averaged $13.62 per cwt for the entire period.

- The market-oriented era (1996-2006). It was during this period that the three-year cycle began to emerge. Supply and demand were in better balance. Real milk prices continued to decline but at a much slower rate of 37 cents per cwt annually. Milk prices averaged $14.73 per cwt for the period, returns improved, and ROE averaged 4.3 percent.

Net cost of production per cwt trended sharply down during both the post-parity and market-oriented eras. Milk production per cow grew 1 to 2 percent per year, spreading fixed costs over more units. Producers adopted technology at a rapid rate, giving economies of scale economic advantages. During the post-parity and market-oriented eras, the U.S. dairy herd decreased from 11 million head to slightly more than 9 million.

- The dairy export takeoff era (2007-2014). While the general economy went into recession in 2008, most U.S. agriculture commodity prices remained unusually strong. The most important driver of strong farm milk prices and returns was the emergence of major export markets.

With two exceptions (2006 and 2009), these years provided producers excellent returns, culminating in 2014 with one of the best years ever. Real milk prices actually increased, with most of the increase in 2014. Milk prices averaged $19.25 per cwt for the entire period. During these eight years, average annual ROE was 6.8 percent.

This era also stands out with a rise in the real (after inflation) cost of production. Corn, soybean and related commodity costs spiked above the rate of inflation in 2007-2013. Higher real milk prices may have made it possible for producers to allow net cost of production to drift upward.

2014: A fluke year

The dairy export takeoff era reached its summit in 2014. Farm Credit East staff suggests the year was a “fluke” created by the perfect storm of a one-time surge in China’s demand for dry milk products coupled with a shortfall of exportable product from New Zealand.

That year, U.S. milk production increased by 5 billion pounds, while farm milk prices increased $4 per cwt and farm profitability reached record highs.

A shift has started

Many of the factors that drove the dairy export takeoff era and culminated with the record year of 2014 have now shifted. A stronger U.S. dollar creates headwinds for exports. China’s buying spree slowed. The European Union (EU) ended production quotas, and New Zealand returned to more normal production.

With those shifts, the U.S. dairy industry has entered a new era. Farm Credit East’s advice: Put 2014 in your rear-view mirror and adjust to changing conditions.

“The sooner the market/industry reset from this period is embraced, the better producers can adjust their businesses to changed realities and prepare for continuing success,” the report stated.

- The Market Pricing Era – V2 (2015-current). Farm Credit East predicts the emerging era will represent a reset of many factors. With milk prices in the $17 to $18 range in 2015, 2016 and likely again in 2017, the current climate appears to be a return to the market-oriented era, including a reduction in farm milk prices and margins.

Instead of holding out hope for a return of 2014, the report suggests the dairy industry turn back the clock to 1996-2010 to view market dynamics. Average net cost of production will be pushed lower, consistently putting farm milk prices under pressure. Farm business rates of return will be significantly lower. Attrition of the national dairy herd and, ultimately, of farms will accelerate.

Those dynamics will require “bold action” to survive and thrive (click here to read How to survive and thrive in a new dairy era). For some producers, that means making substantial adjustments to their cost structure or substantially reducing debt levels to be sustainable.

Low-cost dairy producers will continue to make money, just not as much. Average dairy managers will be continually challenged, and high-cost producers will be under even more intense pressure to either fundamentally improve or to exit the industry. Expansion will be more limited.

The challenge also brings opportunity. Many dairy farms are already well positioned to succeed. Others have the opportunity to make adjustments, but the window of opportunity will not remain open indefinitely. ![]()

Headquartered in Enfield, Connecticut, Farm Credit East is part of the Farm Credit System, providing agricultural credit and affiliated services through 21 branch offices within Connecticut, Maine, Massachusetts, New Hampshire, Rhode Island, New York and New Jersey.

Download the full Farm Credit East Knowledge Exchange Report, Dairy Industry Reset Post-2014: A Time for Dairy Producers to Take Bold Action, at Farm Credit East Knowledge Exchange.

-

Dave Natzke

- Editor

- Progressive Dairyman

- Email Dave Natzke